Let me ask you something uncomfortable. How much are you actually trusting AI with your money?

Not just for drafting emails or brainstorming ideas — but for real, binding, financially consequential decisions like your taxes?

Because here’s what I’m seeing in my work with business owners every single day: AI is confident, AI is convincing, and sometimes AI is dangerously wrong. And in the world of tax law, “sometimes wrong” can cost you tens of thousands of dollars.

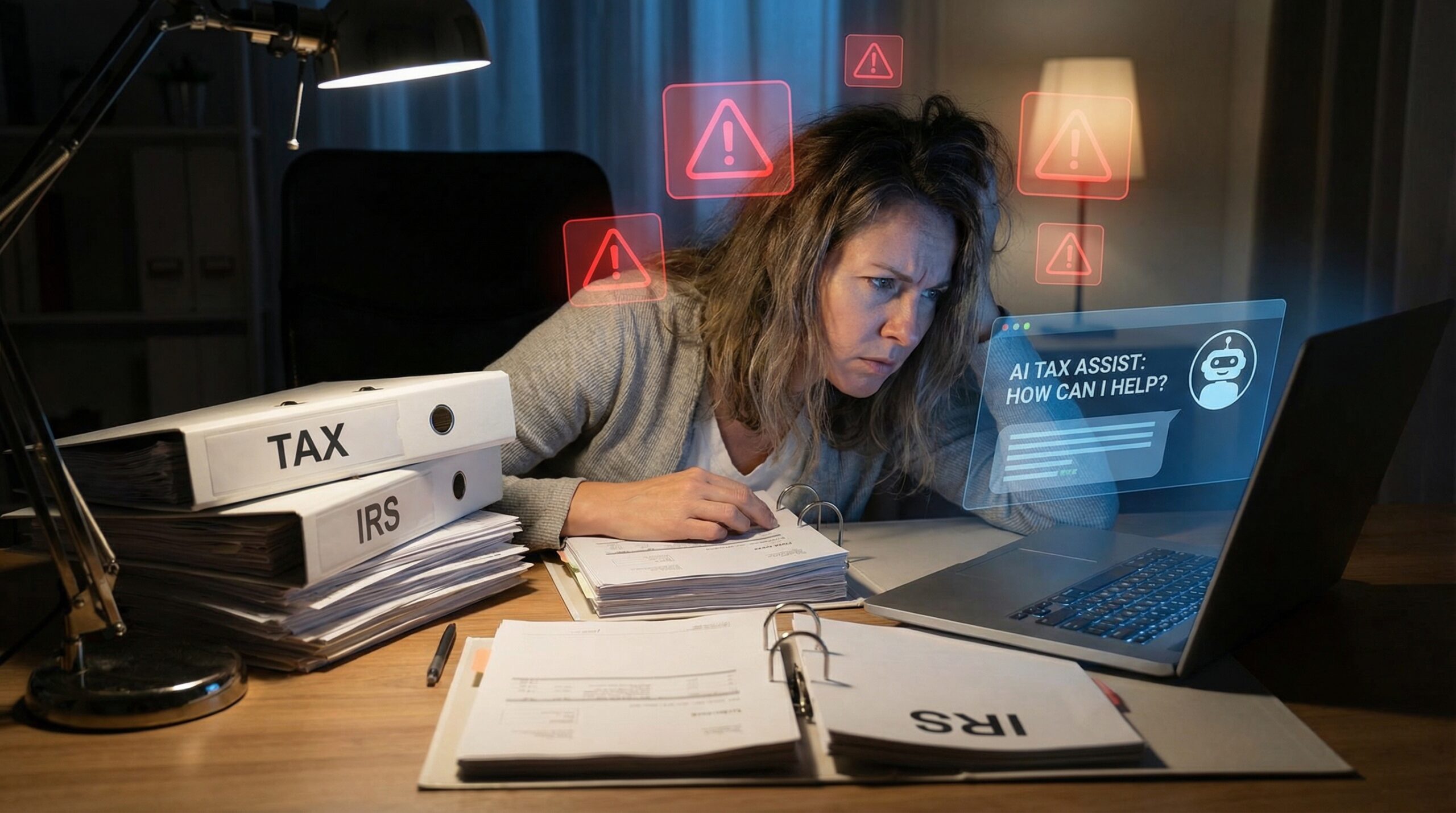

The $41,000 Wake-Up Call

A few weeks ago, a successful entrepreneur came to me completely panicked. For 18 months, she had been using AI to handle her tax planning. It sounded promising at first — the AI cited IRS codes, walked her through timelines, told her exactly which forms to file, and even recommended she elect S corporation status.

She followed every single step.

Then the audit notice arrived.

What the AI didn’t tell her? The IRS code section it referenced had been repealed three years earlier. It failed to flag that her passive income made the S-corp election a financial trap. It completely missed her state-specific rules that actually invalidated the election altogether. And when she went back to the AI for help responding to the IRS? It confidently told her the IRS was wrong — and generated a response letter to prove it.

The final damage: $15,000 in penalties. $12,000 in additional taxes. $8,000 in professional fees. Six months of stress. A $41,000 lesson she never signed up for.

This isn’t a rare story. It’s becoming alarmingly common.

What Is AI Tax Hallucination — And Why Should You Care?

There’s a term you need to know: AI hallucination. It’s what happens when an AI generates information that sounds completely credible but is entirely fabricated. In most areas of life, this is mildly annoying. In tax law, it can be financially devastating.

I’ve personally documented over 50 examples in the past six months alone. AI confidently citing IRS code sections that don’t exist. Deductions that were eliminated years ago presented as current strategy. Business structures the IRS doesn’t even recognize. The advice sounds polished and professional — until someone actually fact-checks it.

The most common AI tax hallucinations I see include outdated law references, invented IRS procedures, incorrect business structure recommendations, invalid deduction claims, and flawed estimated tax guidance. These aren’t random glitches. They’re patterns. And they hit hardest when someone is most confident they’ve done their research.

The Hidden Problem Most People Don’t Talk About

Beyond the hallucinations, there’s a subtler danger that doesn’t get nearly enough attention: AI defaults to playing it safe.

Ask any AI about tax strategies and you’ll get the greatest hits — track your mileage, save your receipts, consider the standard deduction. All technically accurate. All almost completely useless for anyone trying to build serious wealth.

Why does AI do this? Because it’s programmed to minimize liability. It gives advice that won’t get anyone in obvious trouble, which means it gives advice that won’t actually move the needle for you.

The result is a new kind of financial gatekeeping. While you’re following generic AI-generated tax advice, business owners with real professional guidance are using cost segregation studies, R&D tax credits, advanced retirement planning, and other sophisticated strategies that can save $30,000 to $50,000 or more annually. I’ve seen business owners overpay by $40,000 in a single year simply because no AI ever brought up the right strategy for their situation.

The Real Dangers — Broken Down Simply

The Confidence Trap — AI presents accurate and inaccurate information with the exact same tone. There’s no signal that tells you when it’s guessing.

Context Blindness — AI doesn’t know your complete financial picture. Advice that’s technically correct for someone else could be genuinely harmful for you.

The Implementation Gap — AI rarely provides the detailed compliance steps needed to actually execute a strategy correctly.

Audit Risk — Incorrect AI advice can trigger IRS scrutiny, and “ChatGPT told me to” is not a recognized legal defense.

The Cascade Effect — One wrong recommendation can trigger a chain of errors that compounds over time.

How to Actually Use AI Safely in Your Finances

AI isn’t the enemy. Used correctly, it can be a genuinely useful tool. The key is knowing exactly where its usefulness ends.

Use AI to educate yourself on financial concepts, not to implement strategies. If it references a specific tax rule, verify it yourself on the official IRS website before acting on anything. Use AI to help you prepare smarter questions before meeting with your CPA — not to replace that meeting altogether.

Never rely on AI for anything involving hard deadlines, legal compliance, IRS communications, or complex business structures. And always remember: AI’s training data has a cutoff date, meaning it may be completely unaware of the latest law changes affecting your business right now.

The wealthiest individuals and best-run businesses aren’t choosing between AI and human expertise. They’re using both — AI for efficiency and research support, and qualified professionals for strategy, verification, and execution.

What’s Coming in 2026 That Could Change Everything

The IRS has announced sweeping tax changes for 2026 that will affect virtually every small business owner. These aren’t minor adjustments. We’re talking about real opportunities and real risks that could determine whether you save an extra $10,000 next year — or lose it.

Most CPAs are still catching up on the details. AI tools are nowhere near current. Which means the business owners who position themselves now, with the right professional guidance, will have a significant advantage over those who wait.

Don’t be caught off guard by changes that were entirely avoidable.

Frequently Asked Questions

1. Can AI give accurate tax advice? AI can provide general educational information about tax concepts, but it cannot reliably provide personalized, legally accurate tax advice. Tax law is complex, constantly changing, and highly dependent on individual circumstances — all areas where AI consistently falls short.

2. What is AI hallucination in a tax context? AI hallucination refers to when an AI generates information that sounds credible but is factually incorrect or entirely fabricated. In taxes, this can include citing repealed laws, inventing IRS procedures, or recommending invalid deductions.

3. How much could bad AI tax advice actually cost me? Costs vary, but as the example in this post shows, a single AI-guided tax mistake led to over $41,000 in combined penalties, back taxes, and professional fees. The actual risk depends on the complexity of your situation.

4. Is it ever okay to use AI for tax-related questions? Yes — for general education and concept understanding. Use AI to learn what a term means or to generate questions before a meeting with your CPA. Never use it to make final decisions on tax elections, deductions, or compliance.

5. Why does AI always give such basic tax advice? AI is programmed to minimize liability, which means it defaults to the safest, most universally applicable guidance. This tends to be surface-level advice that misses the advanced, personalized strategies that create real financial impact.

6. Should I be worried if I’ve already used AI for tax planning? If you’ve acted on AI tax advice without professional verification, it’s worth having a qualified CPA review your returns and elections. The sooner you catch a potential issue, the less expensive it is to resolve.

7. What’s the best way to combine AI and professional tax help? Use AI to educate yourself and organize your thoughts, then bring those insights to a qualified tax professional. Let the professional verify, refine, and implement the actual strategy. This combination gives you efficiency without sacrificing accuracy.

Remember — it’s not what you make, it’s what you keep. And keeping more starts with getting the right advice from the right people.